Economics can sometimes feel like a dense, jargon-filled world. But understanding key concepts can empower you to make better decisions, whether you’re running a business or just managing your personal finances.

One concept is marginal cost. It’s a fundamental principle that influences pricing strategies, production levels, and even whether a business is going to make it another year or not.

So, what exactly is marginal cost?

Simply put, marginal cost is the change in total cost that comes from producing one more unit of a good or service. It’s not about the average cost of production or the total cost of production, but rather the extra cost incurred by that single additional unit.

Think of it this way: imagine you’re baking cookies. You’ve already made a batch, and you’re considering making a few more. The marginal cost is the cost of the additional ingredients (flour, sugar, chocolate chips) and the additional time and energy needed to bake those extra cookies. It doesn’t include the cost of your oven, which you’ve already purchased.

How to Calculate Marginal Cost:

The formula for marginal cost is quite simple because you’re just calculating the change from producing extra units. Let’s review:

Where:

- Change in Total Cost is the difference in cost after producing additional goods or services.

- Change in Quantity is the increase in the number of units produced.

Let’s break this down with an example:

Imagine a small factory that produces chairs.

- Scenario 1: They produce 10 chairs at a total cost of $500.

- Scenario 2: They increase production to 11 chairs, and the total cost rises to $550.

To calculate the marginal cost of the 11th chair:

- Change in Total Cost: $550 – $500 = $50

- Change in Quantity: 11 – 10 = 1

- Marginal Cost: $50 / 1 = $50

Therefore, the marginal cost of producing the 11th chair is $50.

In essence, you’re looking at the difference in total cost between producing a certain quantity and producing one unit less.

Marginal Cost Calculator:

Below is a marginal cost calculator that I have put together and is free to use. Simply include your email and it will take you to the calculation page.

Once on the calculation page you can use the calculator without needing to actually submit your email (having a 2nd page helps control the spam).

If you do submit your email you will be taken to a private page on my website where you can access and download excel files of all the calculators available today and access a link to the Private Facebook Group to continue the discussion (again, without spam!).

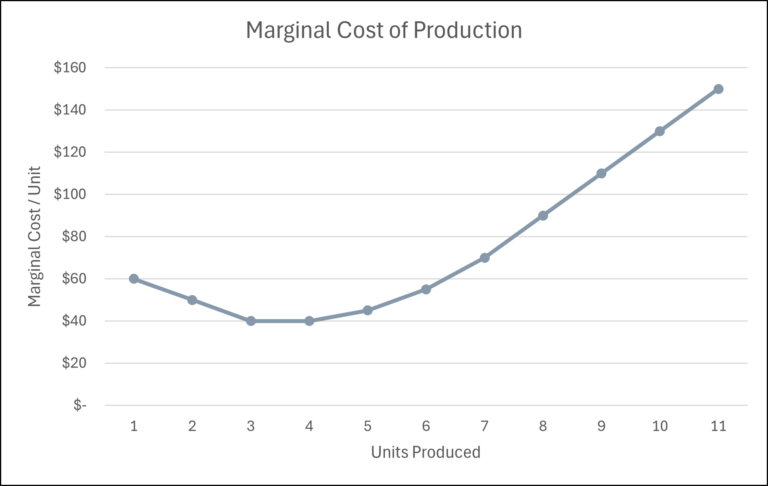

The Slope of the Marginal Cost Curve:

In the chart above, it’s easy to see that the marginal cost curve has a U-shape. Initially, it slopes downwards, before it reaches a minimum, and eventually slopes upwards. Here’s why:

Downward Slope (Increasing Returns)

- In the early stages of production, as a business increases its output, it may experience increasing returns to scale. This means that each additional unit is produced at a lower marginal cost. This could be due to factors like specialization of labor or better utilization of equipment.

Upward Slope (Diminishing Returns)

- As production continues to increase, the business will eventually encounter diminishing returns. This means that each additional unit is produced at a higher marginal cost and is due to the economic theory of diminishing marginal returns. This could be due to factors like limitations of resources, increased coordination difficulties, or the need to hire more efficient workers.

- The slope of the marginal cost curve reflects the rate at which marginal cost is changing as output changes. A steeper slope indicates that marginal cost is changing more rapidly, while a flatter slope indicates that marginal cost is changing more slowly. The point where the marginal cost curve transitions from downward to upward sloping is crucial, as it signifies the point where diminishing returns begin to set in.

Why is Marginal Cost Important?

Understanding marginal cost is crucial for businesses because it directly impacts profitability. Here’s why:

Profit Maximization

- A business maximizes its profit when it produces up to the point where the marginal cost of producing one more unit equals the marginal revenue (the revenue earned from selling that one extra unit). If the marginal cost is lower than the marginal revenue, the business should produce more. If the marginal cost is higher, the business is losing money on each additional unit and should cut back.

- Side Note: I am working on a post for profit-maximizing economics and will post that soon. When I do, I’ll link it here.

Production Decisions

- Marginal cost is critical for businesses trying to decide how much to produce. By analyzing the relationship between marginal cost and demand, businesses can adjust their production levels to meet market needs efficiently.

Short-Run vs. Long-Run

- Marginal cost is primarily a short-run concept. In the short run, some costs are fixed (like rent or equipment), while others are variable (like raw materials or labor). Marginal cost only considers the variable costs associated with producing one more unit. In the long run, all costs become variable, and businesses can adjust all their inputs.

Marginal Cost in Everyday Life:

While we often associate marginal cost with businesses, the concept applies to our personal lives too.

Eating at an All-You-Can-Eat Buffet

- The marginal cost of the next plate of food is practically zero (you’ve already paid for the buffet). This explains why we sometimes overeat at buffets – the perceived low marginal cost encourages us to consume more.

Studying for an Exam

- The marginal cost of studying for one more hour is the value of the other things you could be doing with that time (sleeping, socializing, etc.). You need to weigh the marginal benefit (improved grade) against the marginal cost (lost time).

Driving an Extra Mile

- The marginal cost is the cost of the extra gas and wear and tear on your car. You consider this cost when deciding whether or not to make that extra trip.

Bringing It Home: Why Does Marginal Cost Matter?

Marginal cost is a powerful economic tool that helps businesses make informed decisions about production, pricing, and profitability.

While it might seem complicated at first, understanding the core concept can provide valuable insights into how businesses operate and even how we make decisions in our daily lives.

Next time you’re considering making a decision, think about the marginal cost – it might just change your perspective.